From the founder

This is not a side project. This is the plan.

Nuqsaf starts with one report. The vision is a halal technology platform — banking, cards, and interest-free loans built for observant Muslim households.

The letter

Every year, millions of Muslim households in the West face the same quiet problem. Interest accumulates across savings accounts, brokerage sweeps, CDs, and dividend payments. The obligation to purify is clear. But the math is scattered, manual, and easy to get wrong.

I built Nuqsaf because I was one of those people. I spent hours every year combing through statements, trying to isolate the exact amount. There was no product that did this well — or at all.

Purification reporting is the narrowest, most painful wedge. It is the thing people need solved right now. But it is not the end state.

Once a household trusts Nuqsaf with read-only access to their accounts, the surface area of what we can build expands. Interest-paid awareness. Zakat calculation with visible methodology. Eventually: a financial cockpit for households that want every dollar in their life to align with their values.

The long-term vision is a technology platform. Banking, cards, interest-free loans — a complete halal financial stack where Muslim families can hold money, move money, and grow money. Where the default is halal and the exceptions are visible, not the other way around.

We start small because trust is earned, not declared. Every product decision begins with: does this make the user more informed, or just more engaged? If the answer is engaged, we do not ship it.

This page exists so you know where we are headed. Not all of this is built yet. But all of it is the plan.

Asghar Ali

Founder, Nuqsaf

The roadmap

From one report to a platform.

Each phase builds on the trust earned in the one before it. Nothing ships until the foundation holds.

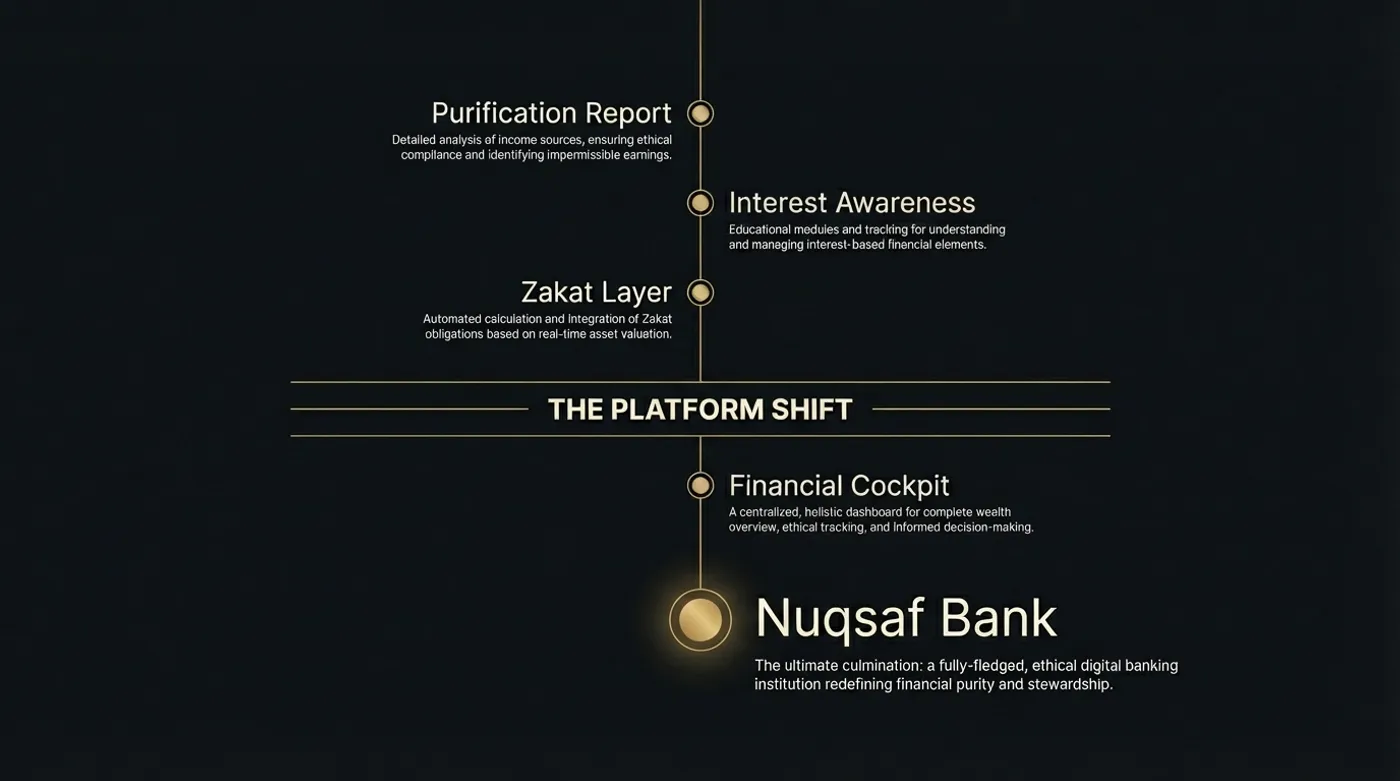

Phase 1 — Now

Annual Purification Report

Connect bank accounts through Plaid. AI surfaces every interest and dividend payment. The user reviews each flagged item. The output is a dated PDF with the exact purification amount, itemized ledger, and methodology stamp.

Trust earned

Read-only access. User controls every decision. Methodology is published.

What unlocks

Account-level transaction history. Understanding of user's financial topology.

Phase 2 — Next

Interest-Paid Awareness

Show users where they are being charged interest — across credit cards, auto loans, student loans, and mortgages. Separate from purification. A clear view of financial leakage that most households never see aggregated.

Trust earned

Nuqsaf understands both sides: what you earned in interest, and what you're paying.

What unlocks

Ability to recommend halal alternatives. Full picture of riba exposure.

Phase 3 — Next

Zakat Support Layer

A careful zakat workflow with explicit assumptions, visible asset classification, and a trail you can review with a scholar. Not a black-box calculator. A structured starting point grounded in the same methodology rigor as purification.

Trust earned

Nuqsaf handles two core financial obligations. Users rely on it annually.

What unlocks

Full asset inventory. Household-level financial planning surface.

The platform shift

Phase 4 — Later

Halal Financial Cockpit

A single surface for ongoing household financial review. Purification history, interest awareness, zakat tracking, and halal alternatives — all in one place. Not a dashboard of vanity metrics. A tool for informed decisions grounded in deen.

Trust earned

Nuqsaf is the financial home for observant households. Deep account access, years of history.

What unlocks

Banking relationship. Users want to move money, not just track it.

Phase 5 — The destination

Nuqsaf Platform

Banking, cards, interest-free loans — a complete halal financial stack. Where the default is halal and the exceptions are visible. Not a fintech wrapper. A technology platform built from the ground up on a framework families trust.

What this means

Banking. Cards. Interest-free loans. Savings. All structured so the user never has to wonder.

Why it works

By the time we get here, every user already trusts Nuqsaf with their full financial picture. The platform is the natural next step.

The thesis

Why this order. Why this slowly.

Trust is the moat. A Muslim household will not give a startup banking access unless that startup has already proven it handles their data, their obligations, and their faith with precision. Every phase earns a specific kind of trust that unlocks the next.

Narrow wedges beat broad launches. Purification reporting is not a big market. That is the point. It is a real, painful, recurring need with no good solution. Solving it well is how you earn the right to solve bigger problems.

The methodology is the product. Anyone can build a dashboard. The hard part is the classification logic, the fiqh-informed rules, and the transparency that lets a user or a scholar verify every decision. That is what makes Nuqsaf defensible.

Informed users are better than engaged users. We do not optimize for time-in-app. We optimize for: does this person leave knowing something they did not know before? That constraint keeps the product honest.

The platform is inevitable if the path is right. If Nuqsaf earns trust with obligations, earns trust with awareness, earns trust with planning — then the question every user will ask is: why am I using financial products that were not built for me?

The first step is live.

Join the waitlist for the annual purification report. See the product. Then decide if the plan makes sense.

Join the waitlist